What is equity release?

Equity release has become increasingly popular in recent years, with over 55s in the UK withdrawing a staggering £3bn from their homes in 2016. In this guide, TechRound is going to explore in further detail about what exactly is equity release, specifically looking at the two main types available: lifetimes mortgages and home reversion.

Equity release explained

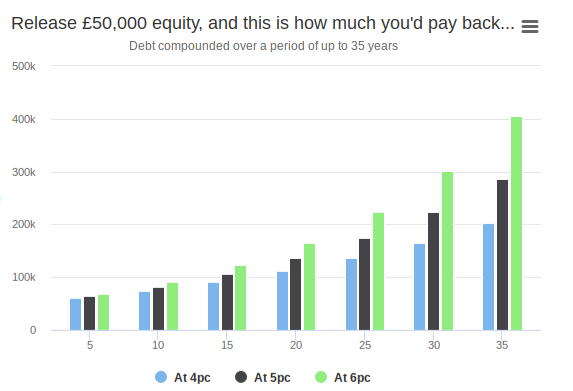

Equity release allows people to unlock money that is tied up in a property. Generally speaking, the amount lenders will allow you to release is usually up to 35% of the property’s value, but the exact figure will depend on your own personal circumstances, and other factors such as your age. For example, a person aged 65 in a house that is worth an estimated £250,000 could be able to release equity of around £80,000. This can be received as a cash lump sum and is often used by homeowners as a way of providing a stable income during their retirement years.

The amount you can borrow will be depend on different factors, certain providers such as Aviva alter the loan based on our postcode. Find more information here.

How equity release works

Equity refers to the exact percentage of the property that you own outright, with equity tending to increase as you get closer to reaching retirement age. Then this amount is released through one of the two main types of equity release, lifetime mortgages or home reversion which is then used for retirement.

There are a number of equity release providers to choose from such as:

- Legal & General

- Aviva

- Pure Retirement

- LV=

- Hodge Lifetime

Who can get equity release?

To be eligible to get equity release there are certain criteria that you will need to have to be able to unlock money in your property. This usually includes the following:

- You will need to be a homeowner of a UK property

- Most equity release companies will need you to be over the age of 55 to qualify for a lifetime mortgage, and at least 60 if you want to apply for the home reversion scheme

- The property that you own will need to be over a specific value. This amount will also be dependent on the company in question.

- Any existing mortgages or secured loans must be paid off first if equity is released. The remaining amount can be used as you wish

The difference between lifetime mortgages and home reversion

We have briefly mentioned the two main types of equity release, lifetime mortgages and home reversion, but what exactly is the difference between the two? We take a further look.

Lifetime mortgages

A lifetime mortgage means that it is secured against your home which then means you can release equity in it and receive a lump sum. With lifetime mortgages you can still benefit if your house increases in value, as well as also retaining ownership of the property.

Home reversion plans

This kind of equity release is when you sell all of your property (or a percentage of it) to a home reversion plan provider in order to release equity from your home, and this is also comes in a cash lump sum. With home reversion plans, you tend to receive a higher lump sum than you would with a lifetime mortgages, but this is partly due to the fact that you have sold some of your house to someone else and therefore lost complete ownership of the property. In addition, you should be aware that if your house increases in value, you will only profit from the percentage of the house you still own.

However, with a home reversion plan, you can still remain in the property, and you will not have to make any repayments in the future, as well as no interest.

Advantages and disadvantages of equity release schemes

Whilst we have broadly covered what the two most popular categories of equity release schemes are, it is worth highlighting the advantages and disadvantages of both of them in order to help you decide whether it may be the right decision for you, or if one is more preferable than the other.

Advantages of lifetime mortgages

- With lifetime mortgages it will still be possible for you to remain in the property

- It could help with reducing the taxable value of an estate, as when the account holder dies, the mortgage is paid with the value of the estate. If the property is below table value after the loan has been paid off, this would mean that inheritance tax would not need to be paid.

- It is possible to borrow money on an as and when basis

- You retain ownership of the property

- You can take out a cash lump sum and use it to live comfortably in retirement

Disadvantages of lifetime mortgages

- If the property loses value, you will still owe a higher proportion of its value

- Taking out a lifetime mortgages means that it will erode inheritance that you have, making it no longer an option

- Age is a factor, as the younger you are the less you can borrow

Advantages of home reversion plans

- When it comes to home reversion plans, it is usually the case that they offer considerably more money than you would otherwise receive with a lifetime mortgage

- It is still possible to give away a percentage of your home as inheritance if you wish to do so

- You can remain in the property

Disadvantages of home reversion plans

- With home reversion plans, if your house increases in value, it will not be possible for you to benefit from this

- Your age, as well as health, will determine the kind of deal or discount that you will get

- You lose all your ownership (or part of it, depending on your particular plan) which means you also lose control over what happens

For the very latest developments in startup news, follow us on more start up news.